The Sri Lankan Island nation thrives on an intricate scheme of taxes that is set about to orchestrate the nation’s development. Here let’s delve into the realm of taxes and tax procedures.

Taxation Principles

The tax landscape in Sri Lanka is built upon foundational principles aimed at fostering economic growth and social welfare, as identified by Adam Smith (1723-1790). The Inland Revenue Act and the Value Added Tax Act constitute the pillars of this symphony, governing over 70% of the Tax threshold and guiding the tax procedures with fairness, equity, and efficiency. The nation’s tax system revolves around direct and indirect taxes, harmonizing with the diverse sectors of the economy.

Functions of Taxes

To explain the Tax system in Sri Lanka, we can provide the 4R functionalities.

Revenue: To fund the infrastructure and administration, and the public services.

Redistribution: Reducing the inequalities

Repricing: Incentivizing or disincentivizing the activities for social wellness.

Representation: Holding the political representatives of a country accountable to the tax citizens for utilizing taxes.

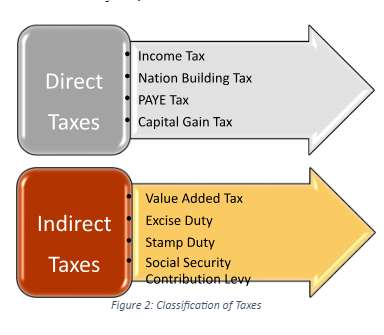

Genres of Taxes

Internationally there are two main genres in taxation. They are;

- Direct taxes: this is of progressive manner and increases according to the earnings. Examples include, PAYE, corporation tax, capital gains tax, etc.

- Indirect taxes: this is of regressive nature which generally applies the same rate for all the people. Examples include VAT, excise tax, customs duty, stamp duty, Social Security contribution Levy (SSCL), Provincial Taxes, etc.

Tax Procedures

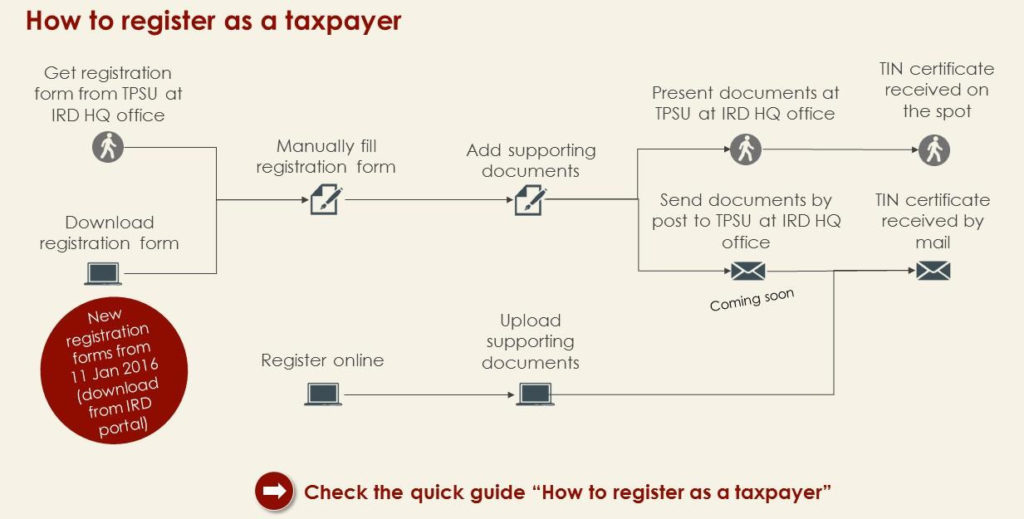

The Sri Lanka Inland Revenue Department (IRD) takes center stage, conducting the fiscal orchestra with precision and transparency. With an emphasis on taxpayer education and compliance, the IRD ensures that the citizens understand their tax obligations and engage in a collaborative effort towards economic development. Any person, either businesses or individuals above the age of 18 can register themselves to be part of this harmonious tax procedure.

A significant aspect of tax procedures is the filing of returns. In Sri Lanka, individuals and businesses are required to submit their income tax returns annually, ensuring the accurate assessment of taxable income. Further, the VAT registered persons should file quarterly returns while payments should be made monthly. This process harmonizes the responsibilities of taxpayers and the government, playing a vital role in the distribution of resources and the provision of public services.

Instruments for the tax procedure

Following are the general requirements to obtain a Tax Identification Number-

- National Identity Card

- Business name registration certificate

- Certificate of Incorporation (if you register as the company)

- Articles of Association (if you register as the company)

- Form 1 (if you register as the company), etc.

Given below are the different tax forms required-

- Income tax return forms

- Estimated tax return forms

- VAT return form

- Tax payment slips, etc.

Tax Benefits

Sri Lanka’s tax process allows certain tax benefits and incentives. The country offers a variety of reliefs, exemptions, and deductions to encourage investment, nurture entrepreneurship, and incentivize economic growth. From export- oriented industries to small and medium enterprises, the Sri Lankan tax system allows for opportunities, empowering businesses and individuals alike.

The Future Taxation Landscape

As the journey through the tax landscape of Sri Lanka draws to a close, the future that lies ahead should be embraced. By adapting to the changing economic dynamics and global trends, the symphony of taxes in the Sri Lankan Island nation continues to evolve. Paving the way for a prosperous tomorrow, Sri Lanka’s tax system strives to promote an environment conducive sustainable development with a focus on simplicity, productivity, and equity.

Conclusion

Sri Lanka pocess a blend of fiscal responsibility, economic growth, and social welfare. The tax procedures play a vital role in shaping the nation’s economic landscape.

This content was facilitated by CeFEnI/COSME and prepared by the University of Sri Jayawardenapura, Kotte

{kind=link}